The April FOMC Paradox: Why a 99% Hold Is the Most Tradable Day of the Quarter

The April 28-29 FOMC carries 99%+ hold odds per the CME FedWatch tool. That sounds boring. It is not. A non-SEP cycle (no fresh dot plot, no updated economic projections) means there is exactly one variable on the tape: Powell's tone. The rate decision is already in the curve. There is no SEP to digest. The entire two-day meeting collapses into a single question — does the Chair lean hawkish, neutral, or dovish in his press conference at 18:30 UTC on Wednesday? Every dollar pair, gold, and the equity tape moves on that one read.

This guide breaks down a structural framework for the day: the volatility split between 18:00 UTC (statement release) and 18:30 UTC (press conference start), a 25-minute bracket method institutional desks have used for years on news events, three Powell-tone scenarios mapped to EUR/USD, USD/JPY, and XAU/USD, and the pattern recognition for when the first move is the real move versus a fake-out fade.

A note on times: all times in this guide are UTC (the default in TradingView and most institutional platforms). The Fed publishes its schedule in Eastern Time -- 14:00 ET for the statement and 14:30 ET for the press conference. That maps to 18:00 UTC and 18:30 UTC during US Daylight Saving (March-November) and 19:00 UTC and 19:30 UTC during US Standard Time (November-March). The April 29 meeting is during DST so the 18:00 / 18:30 UTC schedule applies.

Nothing here is investment advice or a personal recommendation. These are reference frameworks for traders who already understand position sizing and risk management. See our Lesson 1 on systematic versus discretionary trading for the foundation, and our economic calendar for the full week of binary catalysts surrounding this meeting.

- April 29 is a non-SEP meeting -- no dot plot, no fresh projections; Powell tone is the entire trade

- 99%+ hold probability per CME FedWatch -- the rate decision itself is already priced into the curve

- Two distinct volatility windows -- the 18:00 UTC statement and the 18:30 UTC press conference, treated separately

1. The 18:00 vs 18:30 UTC Volatility Split

The single biggest mistake retail traders make on FOMC day is treating 18:00 to 19:00 UTC as one continuous event. It is two distinct windows with very different character. Understanding the split is the foundation of everything else.

The 18:00 UTC release window (the statement)

At 18:00 UTC sharp, the FOMC statement releases. The first 5 minutes are pure algorithmic chaos -- headline scalpers, NLP models parsing word-for-word changes against the prior statement, and liquidity sweeps as market makers reset orders. Spreads widen dramatically. Wicks of 30-60 pips on EUR/USD and $20-40 swings on gold are routine in this window. Trading the first 5 minutes is essentially trading randomness against algorithms with co-located server access -- the retail edge is zero.

From 18:05 to 18:25 UTC -- the next 20 minutes, exactly four 5-minute candles -- the algorithmic noise filters out and institutional flow asserts a direction. This is your Bracket A: the high and low of those four 5-minute candles becomes a structural reference zone. A clean break above the bracket high signals continuation in the bullish post-statement read. A clean break below signals continuation in the bearish direction. Crucially, this trade must complete before 18:30 UTC when Powell starts speaking -- the press conference can blow Bracket A levels apart in seconds.

The 18:30 UTC press conference window (Powell speaks)

Powell's opening prepared remarks usually run 5-8 minutes. The Q&A that follows is where the real volatility lives. From 18:30 to roughly 19:15 UTC, you get Bracket B -- the high and low of the first 25 minutes of Powell speaking. Powell can confirm the statement read, walk it back, or pivot entirely depending on a single question from a Bloomberg or Reuters reporter.

Bracket B almost always overrides Bracket A. If the statement read bullish dollar but Powell sounds dovish in Q&A, Bracket A breaks invalidate and Bracket B sets up the real move in the opposite direction. Traders who already exited Bracket A before 18:30 UTC are positioned to take Bracket B fresh. Traders still holding Bracket A through 18:30 UTC typically get stopped out by the press-conference whipsaw.

- Skip the first 5 minutes after 18:00 UTC -- pure algorithmic chaos, zero edge for retail

- Bracket A = 4 candles from 18:05 to 18:25 UTC -- bracket-break trades must complete before Powell speaks at 18:30 UTC

- Bracket B = first 25 minutes of Powell, 18:30 to 18:55 UTC -- overrides Bracket A and is where the real directional move usually lives

2. The Three Powell Scenarios

Every FOMC press conference reduces to one of three tone reads. Knowing which scenario you are in tells you which side of the bracket break is the higher-probability follow-through.

Scenario A: Hawkish Hold

Powell sounds hesitant to cut. Phrases to listen for: "inflation is still above our 2% target", "we need more confidence", "we are not in a hurry", "the labor market remains tight". If multiple phrases like these stack inside the first 15 minutes of Q&A, the curve reprices cuts further out, the dollar bids, real yields rise, and gold sells off. Bracket B break to the upside on the dollar corresponds to the bracket break down on gold and EUR/USD.

Scenario B: Neutral / Mechanical Hold

Powell sticks tightly to the statement language with no additional color. Phrases to listen for: "data-dependent", "meeting by meeting", "we will continue to monitor". This is the flat scenario -- bracket setups often fail to generate sustained breaks in either direction, ranges compress, and the day closes without a meaningful trend. The right call is often to stand down and wait for Thursday's PCE print or Friday's NFP for clearer macro direction.

Scenario C: Dovish Hold

Powell signals openness to cutting. Phrases to listen for: "progress on inflation has been notable", "the labor market has cooled", "we are getting closer", "a cut at the next meeting is possible". The curve adds June or September cut probability, the dollar sells off, real yields fall, and gold catches a strong bid. Bracket B break to the downside on the dollar = bracket break up on gold and EUR/USD.

- Hawkish Hold -- DXY up, gold down, EUR/USD down, USD/JPY up

- Neutral Hold -- ranges compress, often a stand-down day; revisit after PCE / NFP

- Dovish Hold -- DXY down, gold up, EUR/USD up, USD/JPY down

3. Per-Asset Reaction Map

Different assets react to different parts of the FOMC tone. Knowing which lever an asset pulls on lets you read the brackets in the right direction once a Powell scenario is clear.

EUR/USD -- relative monetary stance

EUR/USD is fundamentally a relative trade between Fed and ECB stance. The ECB cut through 2025 and into Q1 2026; the Fed is on hold. A hawkish Powell hold widens the policy gap and pressures EUR/USD lower. A dovish hold narrows the gap and EUR/USD rallies. Key reference zone for the April 2026 meeting: traders watching the 1.1480-1.1520 zone as the structural pivot -- a sustained Bracket B close above signals dovish continuation, a sustained close below signals hawkish.

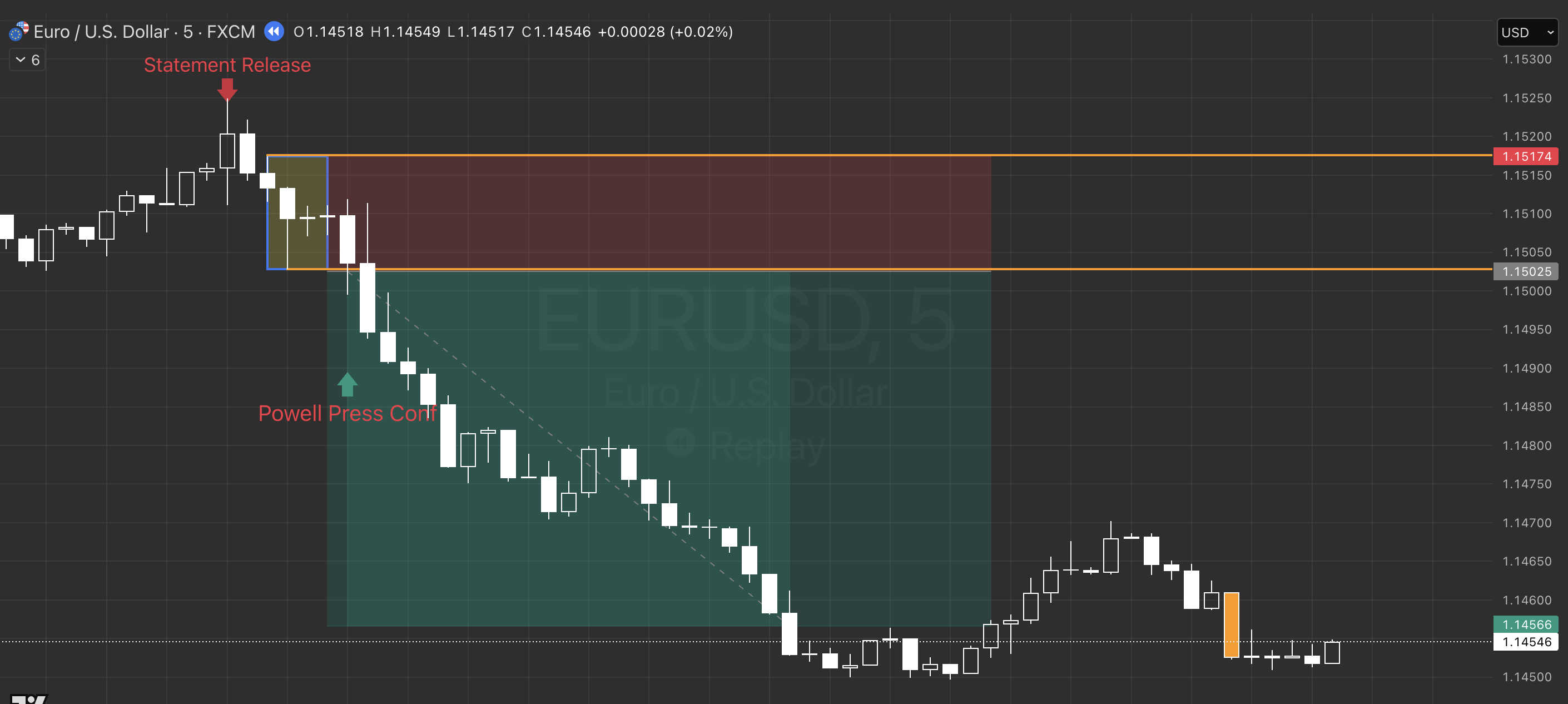

Worked example -- March 18 2026 FOMC, EUR/USD 5-min: the bracket high formed at 1.15174, the bracket low at 1.15025 (the highest and lowest wicks across the four candles 18:05-18:25 UTC). Price broke below the bracket low and rolled over into Bracket B as Powell's tone reinforced the bearish read. Structural exit on a change of character (CHoCH) about 2h 35m later delivered roughly 3x the bracket-height risk distance. The chart below marks the statement release, the 4-candle bracket, the bearish break, and the held trend through Powell.

USD/JPY -- US Treasury yields

USD/JPY is the closest thing to a pure US 10-year yield play in FX. Hawkish Powell = yields up = USD/JPY up. Dovish Powell = yields down = USD/JPY down. Japan is hyper-sensitive to the rate differential because the BoJ remains effectively at zero. Key reference zone: 156.50-157.00 as the structural pivot for the April meeting reaction.

XAU/USD (Gold) -- US real yields

Gold is the cleanest expression of US real-yield direction (10-year Treasury yield minus 10-year breakeven inflation). Hawkish Powell = real yields rise = gold falls. Dovish Powell = real yields fall = gold rises. With gold consolidating near $4,710-$4,726 into the meeting, the structural reference levels are $4,650 (bearish trigger if Powell hawkish) and $4,780 (bullish trigger if Powell dovish). Realised 24-hour ranges on FOMC day routinely exceed $40-60 on gold.

- EUR/USD -- Fed-vs-ECB relative stance; pivot zone 1.0820-1.0850

- USD/JPY -- US 10-year Treasury yields; pivot zone 156.50-157.00

- Gold (XAU/USD) -- US real yields (10y nominal minus 10y breakeven); pivot zones $4,650 (bearish) and $4,780 (bullish)

4. When the First Spike Fades -- Pattern Recognition

Not every initial move is the real move. Knowing when to trust the first spike versus when to fade it is the difference between catching the day's directional move and getting chopped up. Three patterns to watch:

The Statement-Powell Conflict

The FOMC statement reads hawkish (or dovish), price spikes one way for 5-10 minutes, and then Powell's press conference contradicts the statement read. The first spike fades hard, often retracing the entire move and continuing in the opposite direction. This happens roughly 30% of FOMC days and is the single highest-conviction fade pattern. The tell: Powell's first 3-5 minutes of prepared remarks -- if his framing diverges from the statement language, the fade is on.

The Liquidity Sweep

Within the first 5 minutes after 18:00 UTC, price runs aggressively in one direction to sweep stop clusters above or below recent swing highs/lows, then reverses sharply. This is algorithmic stop-hunting, not real flow. The tell: the sweep candle prints abnormal volume relative to the next 2-3 candles, and price closes back inside the prior range. Bracket A confirms or denies the sweep direction within 25 minutes.

The Continuation Confirmation

The first move IS the real move when three things stack: (1) a clean break of a structural level on the 18:05 UTC candle, (2) Bracket A holds the break through all four candles without a deep retest, and (3) Powell language reinforces the direction in his first 10 minutes. When all three align, fade attempts get steamrolled. This confluence usually only confirms by 18:25-18:30 UTC, which is exactly when Bracket A trades resolve.

- Statement-Powell conflict -- when statement and press conference diverge, the first spike fades violently (~30% of days)

- Liquidity sweeps happen in the first 5 minutes -- abnormal-volume reversal candle is the tell

- Real-move continuation needs three confluences: clean break, Bracket A holds without retest, Powell reinforces direction

5. Risk-Management Ground Rules

FOMC days are high-volatility events where typical risk parameters need adjustment. Several baseline rules used by systematic desks:

- Position size halved -- implied volatility runs 2-4x normal in the bracket windows; the same nominal size carries 2-4x the dollar risk

- Spread awareness -- EUR/USD spreads can widen from 0.1 pips to 2+ pips at the 18:00 UTC release; gold spreads from $0.20 to $1.50+. Limit-order behaviour changes accordingly

- No new positions during the gap -- between 18:25 and 18:30 UTC, when Bracket A has just resolved and Bracket B has not started, is the worst time to be opening fresh exposure

- Pre-defined invalidation only -- the structural invalidation level (opposite bracket extreme) is set before the bracket break, never adjusted as price moves

- Single-event maximum loss cap -- many systematic desks set a per-event max loss equal to 1-1.5x normal daily risk; FOMC carries enough tail risk to justify the hard cap

None of this is investment advice. These are baseline operational practices used by traders who treat FOMC as a high-volatility event rather than a normal session. New traders should consider standing down entirely for the live event and reviewing the day's price action in retrospect rather than trading it.

- Halve position size on FOMC days -- implied vol is 2-4x normal

- Watch spreads -- they widen meaningfully and affect limit-order behaviour

- Pre-defined invalidation only -- no moving the structural risk reference once the bracket breaks

6. The April 29 2026 Specifics

For Wednesday's specific meeting, three context points matter for the framework above:

Statement timing -- 18:00 UTC. Bracket A runs 18:05-18:25 UTC. Powell press conference begins 18:30 UTC. Bracket B runs 18:30-18:55 UTC. (For US-time readers: that's 14:00 ET / 14:30 ET respectively. Set your TradingView default timezone to UTC so the markings match the framework one-to-one.)

Pre-meeting positioning. The DXY is consolidating after a multi-month range, gold sits at $4,710-$4,726 after a pullback from the $5,000 cycle high earlier in March, and BTC is wedged between $75,000 and $80,000. ES futures printed a record S&P close at 7,165 on Friday April 25. The setup is compressed, which historically delivers larger post-FOMC moves than weeks where positioning is already extended.

Tail risk to the day. Microsoft, Meta, Alphabet, and Amazon all report earnings after the close on the same Wednesday. Equity-driven flow into the close can override Bracket B in equity-index futures. FX (EUR/USD, USD/JPY) and gold are cleaner reads of the FOMC alone because they are less reactive to single-name earnings.

For the broader week-of structure see our Monday morning analysis, and the full economic calendar for Tuesday-Friday catalysts including PCE on Thursday and NFP on Friday.

- Bracket A 18:05-18:25 UTC, Bracket B 18:30-18:55 UTC -- mark the exact UTC times in your charting software the night before

- Compressed pre-meeting positioning historically delivers larger post-FOMC moves

- Mag 7 earnings overlay -- equity-driven flow can override Bracket B in indices; gold and FX stay cleaner reads

Closing Note

The bracket framework is structural, not predictive. It does not tell you which way price will go -- it tells you where the high-probability levels for a directional break are, and gives you a defined invalidation point on the opposite side. The Powell-tone scenario read tells you which direction is the higher-probability break once a scenario becomes clear. That is the entire framework: structural levels for risk, scenario read for direction, discipline to wait for both before acting.

Most retail traders lose money on FOMC days because they trade the statement-release spike with no framework, get stopped out in the algorithmic chaos, and then can't bring themselves to take the real Bracket B move when Powell finally clarifies the tone 30 minutes later. Knowing about the two windows in advance is half the battle.

For the daily structural reads on individual assets across this week, see our market insights feed. For the systematic foundation that makes any of this tradeable in the first place, start with our free trading course.