The Week in Summary

April 6-12 delivered the most consequential macro event of the quarter: a U.S.-Iran two-week ceasefire that crashed oil 14%, powered the S&P 500 to its best week since November, and allowed Bitcoin to shake off a weeks-long stretch of extreme fear. The relief is real -- but fragile. The ceasefire began fraying within 24 hours, the Strait of Hormuz backlog sits at 800+ vessels, and next week's JPMorgan earnings will test whether corporate America is pricing the geopolitical reset or still hedging it.

Story 1: Oil -14% -- The Ceasefire and What It Really Means

The week's defining trade happened on a single headline. On Tuesday evening, just 90 minutes before Trump's stated deadline for strikes on Iranian infrastructure, Pakistan-brokered negotiations produced a two-week ceasefire. Iran agreed to partially reopen the Strait of Hormuz; the U.S. agreed to suspend planned operations for the duration.

WTI crude collapsed 16.4% in a single session -- from $112 to $94.41 per barrel, the largest one-day oil decline since 2020. By Thursday, Iran accused the U.S. of three violations: continued Israeli strikes on Lebanon, an unidentified drone in Iranian airspace, and Washington's refusal to formally acknowledge Iran's enrichment rights. Oil bounced back to $97.33 before settling near $95.50 by week's end. Energy stocks -- Exxon, Chevron, Occidental -- shed 5-7% on the session and finished the week negative.

The net result: a 14% weekly decline and a new market equilibrium. The ceasefire has not resolved the conflict; it has reset the war premium from $112 to a new range of $90-105.

- WTI at $95.50 -- down 14% on the week, largest weekly drop since the pandemic demand shock

- Ceasefire fraying by Thursday -- oil remains headline-driven; any Iran news can move it 2-5% instantly

- 800+ vessel backlog in Hormuz -- supply normalization takes months even with a durable deal

- $90-105 is the new trading range -- markets are no longer pricing worst-case, but no clean resolution either

Story 2: S&P 500 Posts Best Week Since November

The S&P 500 gained 3.6% to close Friday at 6,817 -- its best weekly performance since November 2025. The Dow surged 1,325 points on April 8 alone (its best single-day gain in over a year) and the Nasdaq rose 2.8%. The global rally was equally broad: Japan's Nikkei soared 5%, South Korea's Kospi surged 7%, and European indices gained 2.5-3.8%.

The week was powered by three overlapping tailwinds: falling oil reducing near-term inflation expectations, a core CPI print below forecast, and continued strength in tech and AI names. The energy sector was the lone major loser, dropping sharply as crude crashed. Airlines and travel stocks surged early in the week on cheaper-fuel optimism before partially retracing as oil bounced Thursday.

- S&P 500 at 6,817 -- +3.6% on the week, best performance since November

- Dow's best single-session gain in over a year (April 8, +1,325 points)

- Tech and AI led; energy sector the sole major loser -- a clean barometer of the oil re-pricing

- S&P 6,700 is key support -- holding it going into earnings season keeps the recovery thesis intact

Story 3: Gold Holds Near $4,765 -- Volatility Beneath a Stable Surface

Gold's 1.7% weekly gain (from $4,686 to $4,765) understates a wilder intraday path. On April 8, spot gold briefly spiked to $4,888 -- a near three-week high -- as the ceasefire triggered simultaneous relief-asset and risk-on positioning. By Thursday, as the ceasefire cracked and oil bounced, gold pulled back to $4,716. It consolidated near $4,750-4,765 through the weekend.

The structural case for gold has not changed. Central bank purchases are running at multi-year highs, dollar reserve diversification continues, and the Fed's path toward eventual rate cuts remains the base case. The first month where energy disinflation shows up in CPI will be April data, releasing in mid-May -- a potential major catalyst. For gold's key technical levels in detail, see our April 9 morning analysis.

- Gold at $4,765 -- +1.7% on the week; intraday range of $4,688 to $4,888

- $4,800 is the level to break for a retest of recent highs near $4,858

- Central bank demand unchanged -- the weekly pullback is a consolidation, not a trend break

- May CPI will be the first reading that captures oil's post-ceasefire drop -- watch for it

Story 4: Bitcoin Shakes Off Extreme Fear, Closes Near $73,000

Bitcoin's recovery this week was one of the strongest signals in risk assets. BTC started the week near $67,043 with the Crypto Fear & Greed Index at 12 (Extreme Fear), climbed to $72,841 on the April 8 ceasefire rally -- triggering $600 million in short liquidations -- then held above $71,000 when the truce frayed Thursday. By the weekend it consolidated near $72,978. Ethereum tracked the move, recovering from $2,044 to $2,187 (+7.0% on the week).

The key signal is the divergence: Fear & Greed remains pinned at 12-16 (Extreme Fear) even as prices have recovered meaningfully from the $64,000-65,000 March lows. When price rises and sentiment stays deeply negative, institutional accumulation is typically the explanation. ETF inflows continued throughout the week, and on-chain data shows long-term holder wallets increasing positions during each dip.

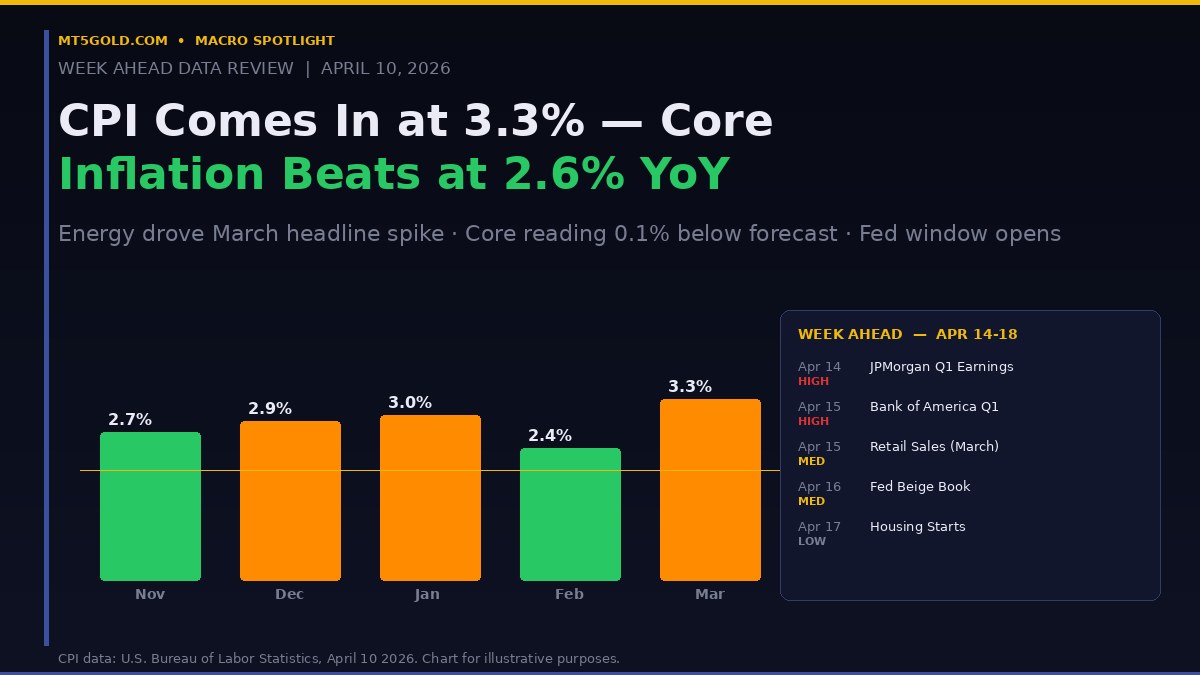

March CPI came in at 3.3% YoY -- driven almost entirely by gasoline. The week ahead brings JPMorgan Q1 earnings and Retail Sales.

- BTC at $72,978 -- +8.9% on the week, well above the $70,000 key support floor

- ETH at $2,187 -- +7.0% (wk), recovering from March lows near $1,900

- Fear & Greed at 12-16 while price recovers -- a classic institutional accumulation signal

- $70,000 is the critical level -- losing it would signal the rally is failing; holding it extends it

CPI 3.3% -- Energy Drove the Spike, Core Held

Friday's CPI release showed March headline inflation at 3.3% year-over-year -- in line with the Dow Jones consensus -- driven almost entirely by energy. Gasoline surged 21.2% in March, accounting for nearly three-quarters of the headline increase. The constructive detail: core CPI came in at 2.6% YoY and 0.2% MoM, both 0.1 percentage point below consensus forecast.

The critical nuance: March CPI reflects oil prices before April 8's ceasefire. The 16% crude crash that day will not appear until the April CPI, releasing in mid-May. The Fed is reading backward-looking data through a forward-looking lens -- and the below-consensus core print gives it room to maintain patience. Rate-cut odds ticked slightly higher after the release.

- Headline CPI: 3.3% YoY -- in line with consensus, driven by gasoline (+21.2%)

- Core CPI: 2.6% YoY / 0.2% MoM -- 0.1pt below forecast; the constructive detail in the report

- March reflects peak oil prices -- the April data (mid-May release) will show the ceasefire effect

- Fed has room to stay patient -- core below consensus keeps the rate-cut window open for late 2026

Week Ahead: JPMorgan Earnings, Retail Sales, Fed Beige Book

The most consequential week for Q1 2026 corporate data begins Monday. JPMorgan Chase reports before the opening bell on April 14 -- consensus expects revenues of $48.2B (+6.4% YoY) and net interest income of $25.6B (+10.1%). The real signal will be management commentary on the 2026 economic outlook and investment banking pipeline, not the headline EPS number. Bank of America follows on April 15, the same morning as March Retail Sales (consensus +0.3% MoM), creating a double-catalyst morning for consumer and credit trends.

The Fed Beige Book drops Wednesday April 16 -- the first regional economic picture that may capture how Iran-conflict disruptions and the ceasefire affected business sentiment in real time. Housing Starts follow Thursday April 17, a test of whether the lower oil-driven inflation expectations are translating into mortgage rate relief for buyers.

- Mon Apr 14 -- JPMorgan Q1 Earnings (pre-market): Revenue seen $48.2B; IB commentary is the real signal. IMPACT: EXTREME

- Tue Apr 15 -- Bank of America Q1 + Retail Sales: Credit quality + consumer spending back-to-back. IMPACT: HIGH

- Wed Apr 16 -- Fed Beige Book: First post-ceasefire regional picture; watch business sentiment language. IMPACT: MEDIUM

- Thu Apr 17 -- Housing Starts: Test of lower-inflation mortgage rate pass-through. IMPACT: LOW-MEDIUM